Publish Date

Jul 24, 2023

Industry Insights

To provide an interim update on key themes and trends we previously identified for this AGM season, we have analyzed an initial sample of the first FTSE 350 companies to report this year.

Our sample includes approximately 50 companies, representing around one fifth of the FTSE 350 (excluding investment trusts), evenly split between the FTSE 100 and FTSE 250.

We have analysed practice in three key areas:

Last year, salary budgets faced increased pressure due to rising inflation and the cost-of-living crisis. As we outlined in November in our article Executive director salary increase: to align or not to align?, in 2022, there was a growing trend among companies to adopt a ‘discounted’ approach for executive director salaries, where the percentage increase was below the average for the wider workforce. This contrasted with the previously well-established practice to align with the average employee rate and reflected evolving shareholder expectations for greater restraint. At the start of 2022, only around a fifth of the market was discounting. This had risen to over half of the market by mid-year, and we anticipated this trend to continue in 2023.

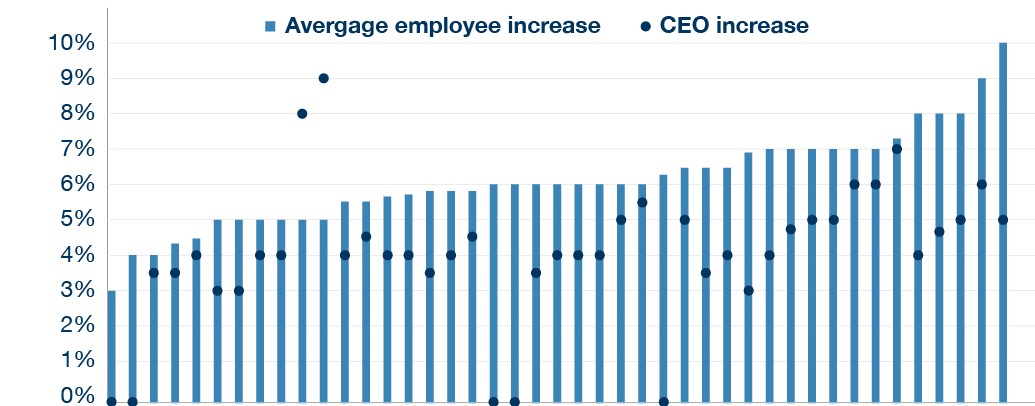

Analysis in our sample indicates that the trend has indeed continued into 2023. The following chart illustrates market practice in the group, showing both the average employee and the CEO salary increase (with each bar and associated marker representing one company).

This year, the median increase for the average employee stands at 6.0 percent (compared to 4.4 percent last year), with most companies ranging from 5 to 7 percent. These figures are likely driven by factors such as sector dynamics, talent market trends, and business circumstances (affordability, etc.). In some cases, companies have adopted a ‘tiered’ approach for their wider workforce, focusing on higher increases for junior colleagues, although detailed disclosure of this approach is often not provided. Additionally, many companies have offered additional one-off support payments to lower paid employees.

As anticipated, the adoption of a discounted approach for executive director salary increases has become almost universal practice (with only two outliers in the sample). However, the question arises: How should one interpret the market data regarding the relative positioning of the CEO increases compared to those all-employee reference points?

Combining these observations suggests that there is some ‘relativity’, such that we might expect higher all-employee increases to correlate with higher CEO increases, but with companies taking a robust and responsible approach by applying greater discounts for executive directors for larger all-employee increases.

It is difficult to predict how the environment will evolve. Should inflation remain persistently high, and in excess of salary increases awarded during 2022 and 2023 to date, we would expect continued pressure on salary budgets for the remainder of 2023 and into 2024. In this scenario, while many shareholders may expect remuneration committees to continue to show restraint and adopt a discounted approach for executive directors, doing so over a sustained period jeopardizes the market competitiveness of the package. Conversely, should inflation recede and all-employee salary budgets return to the previous norm of c.2-3 percent, we expect market practice to return to aligning executive directors’ increases with those levels.

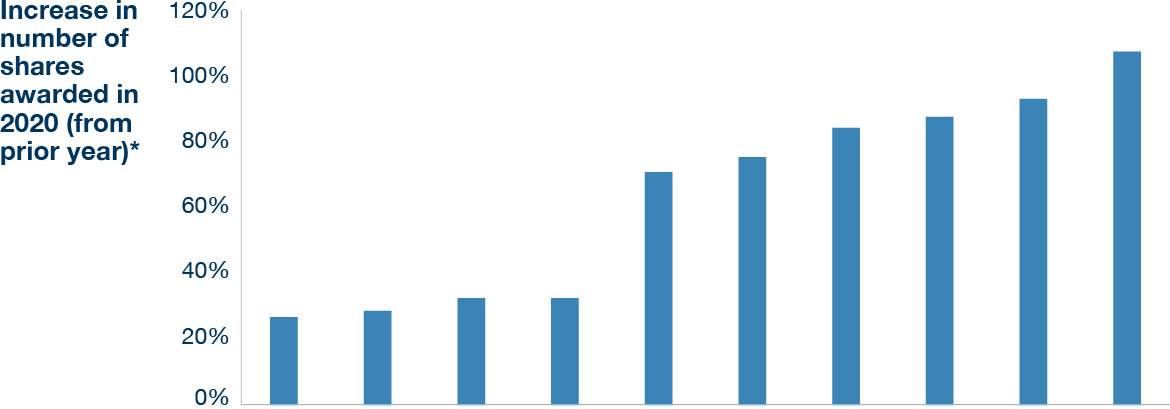

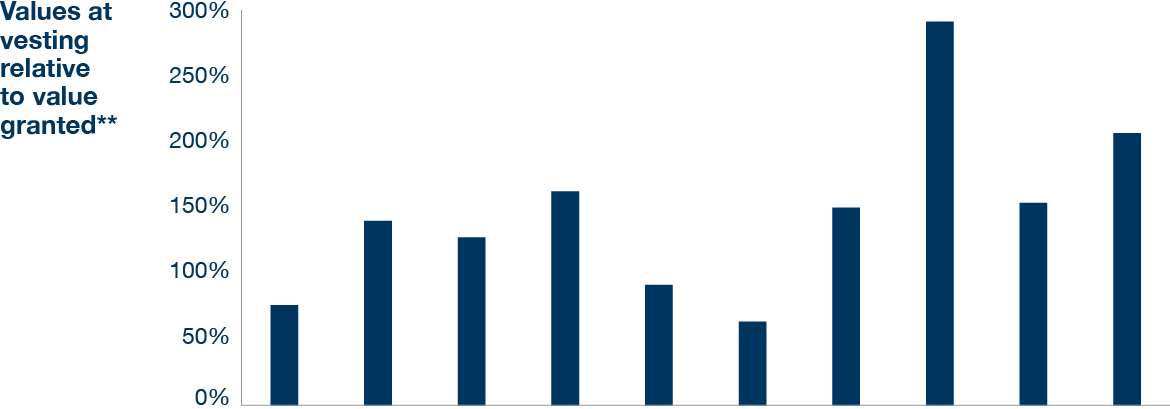

We anticipated that ‘windfall gains’ would be one of the key themes of this year’s AGM season. To recap, for companies that granted long-term incentive awards (LTIPs) in 2020 using share prices that had been significantly reduced due to the COVID-19 pandemic, (such that a higher number of shares had been awarded compared to the previous year), shareholders expected the remuneration committee to assess if a ‘windfall gain’ had transpired upon vesting. For more information, please refer to our comprehensive report ‘Windfall Gains: Your Guide‘ published in January 2023

For most companies in our sample, the issue is unlikely to have been relevant in practice due to their specific circumstances, such as the share price trajectory pre or post grant in 2020 and/or the non-vesting of the LTIP award.

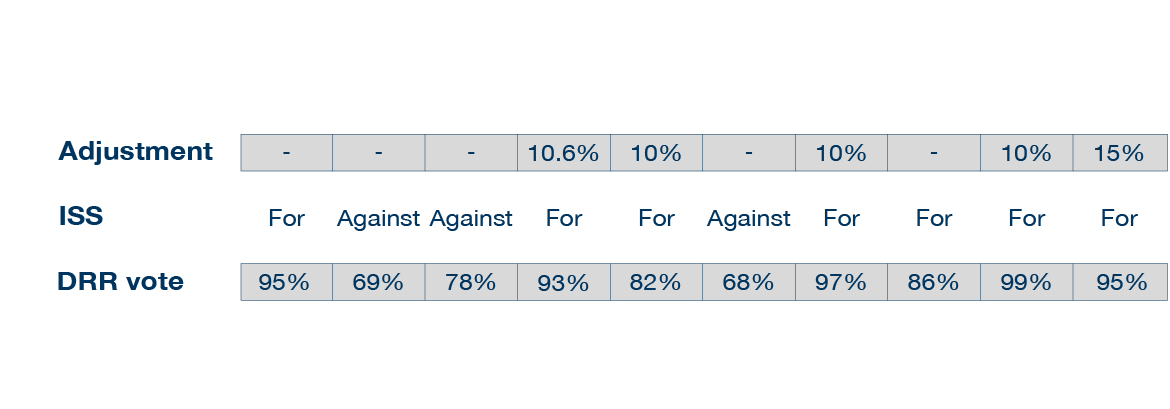

However, for around a quarter of the sample, it may have been a relevant consideration. These companies are depicted in the charts below, which present relevant data points for the companies (each bar represents one company, maintaining the same order on each chart). The first chart illustrates the increase in the number of shares granted in 2020 (i.e. as a result of share price decline pre-grant). The second chart displays the share price performance post-grant (combined with the level of award vesting). Additionally, the charts include information on the level of windfall gains adjustment at vesting (if any), the ISS recommendation and the DRR vote.

We make the following observations:

Setting performance targets, for both short and long-term incentives, remains a key activity in the annual cycle of remuneration committees. Balancing the interests of all stakeholders and ensuring that targets satisfy shareholder expectations while being fair and achievable for management has always been challenging. This task has become even more difficult in the current period of prolonged uncertainty.

To assist remuneration committees and reward teams in this task, we developed the 2023 Target Setting Toolkit. This toolkit provides a range of market reference points on performance targets for profit metrics within both the annual bonus and long-term incentives. It provides a comprehensive analysis of companies across the FTSE 100, FTSE 250, and FTSE Small Cap.

Due to the smaller sample size in this context, it is not practical or appropriate to reproduce that full analysis from the Toolkit. However, we can make some observations on key trends from our sample:

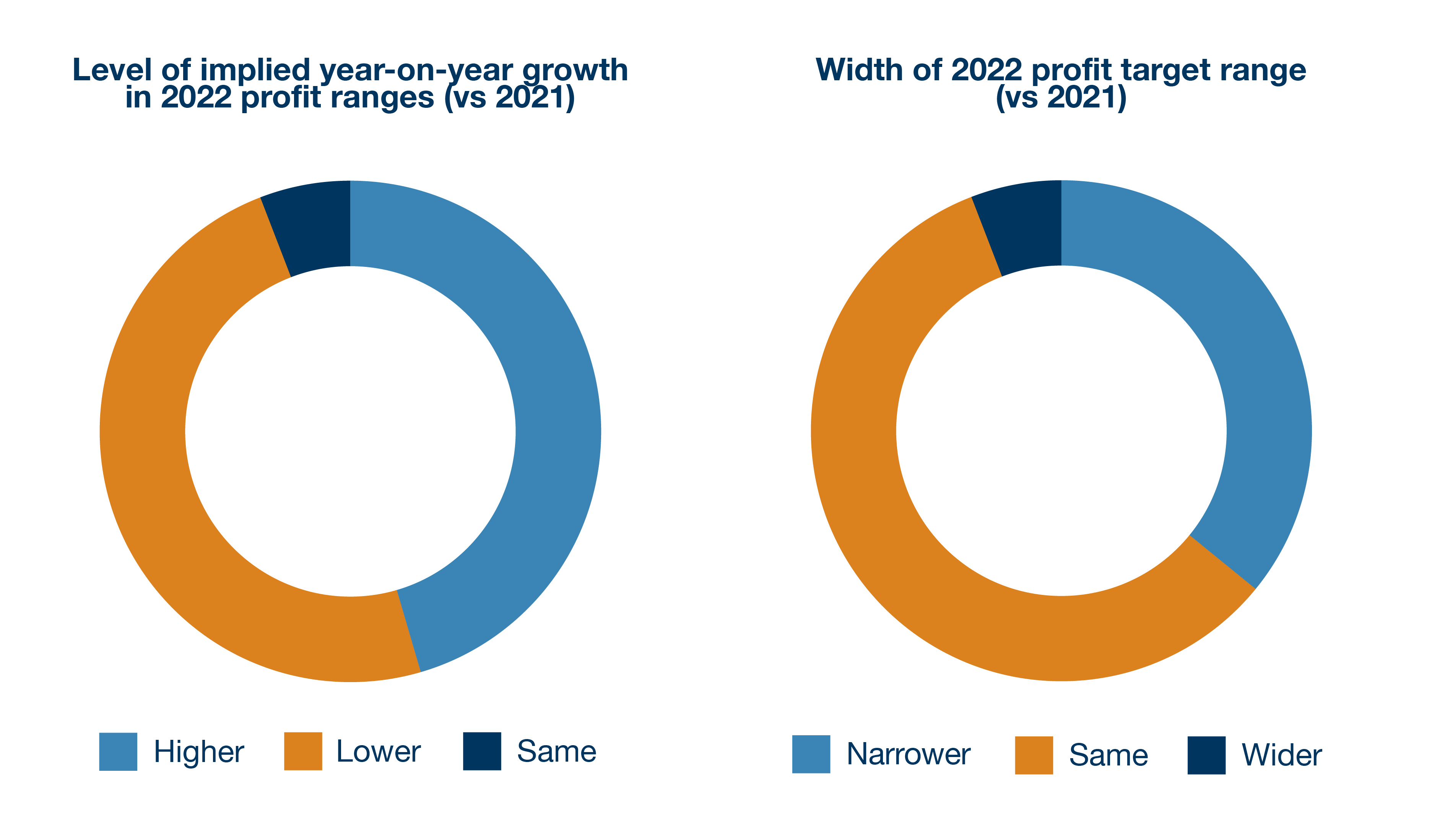

We can compare the profit targets in annual bonus plans for the reporting year (i.e. 2022) against those in the same company for the prior year (2021), and observe that:

There was a broadly even mix between companies that increased and those that decreased the required year-on-year level of growth in the target ranges. This is perhaps to be expected as companies calibrate their ranges to their specific circumstances. However, given the relatively high level of bonus outcome seen in 2021, we might have anticipated more companies to increase the stretch in their bonus targets for 2022.

There was a clear trend towards narrowing the profit target ranges for 2022. This shift can be attributed to companies aiming for a ‘return to normal’ after widening the ranges in 2021 to account for the uncertainty caused by the ongoing impact of the COVID-19 pandemic.

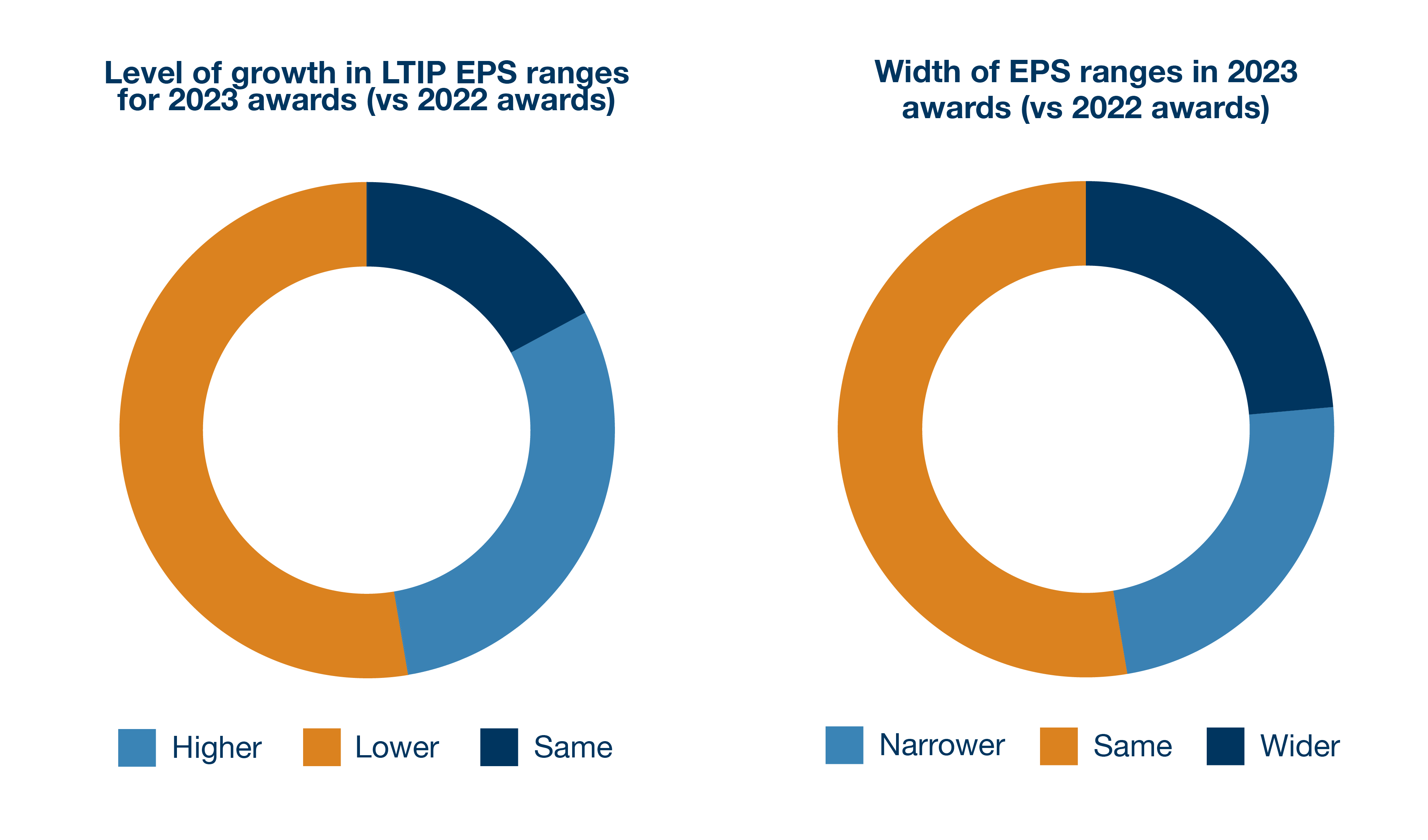

Similarly, we can examine the profit targets in LTIP incentive awards, although the timing differs slightly from the bonus targets above. In this case, we compare the disclosed approach for awards to be granted in the year ahead (i.e. 2023) with those in the same company for the reporting year (2022).

Most companies reduced the level of EPS growth in their 2023 EPS target ranges compared to that in last year’s awards. This reduction likely reflects ongoing concern around the global macroeconomy and growth prospects. It could also be influenced by some companies having higher ‘base year’ EPS for these awards compared to awards from the previous year.

Regarding the width of ranges in the LTIP EPS targets, most companies made no changes. However, among those that did, there was a fairly even split between companies that widened and those that narrowed the range.

Target setting is likely to remain one of the most challenging areas for remuneration committees, particularly as the level of uncertainty shows no immediate signs of improving. A formulaic solution is unlikely to exist, therefore judgement is required. We strongly encourage remuneration committees to exercise informed judgement when calibrating performance ranges, taking into account various factors and reference points, and following a sound process as outlined in our published Toolkit.

https://www.alvarezandmarsal.com/insights/2023-agm-season-ftse-350-companies-trends-and-observations