Publish Date

Apr 05, 2023

A&M Tax Advisor Weekly

On March 15, 2023, the Financial Accounting Standards Board (FASB) published a proposed Accounting Standards Update (ASU), “Income Taxes (Topic 740): Improvements to Income Tax Disclosures,” aimed at providing greater transparency into entities’ global operations. The proposed amendments seek to enhance disclosures providing more useful information to users regarding the effective tax rate and statement of cash flows. In addition, the ASU addresses several other areas that had been previously exposed for public comment. These disclosure changes will provide for more extensive disclosure requirements as well as additional control considerations for Companies as they seek to implement.

Public entities

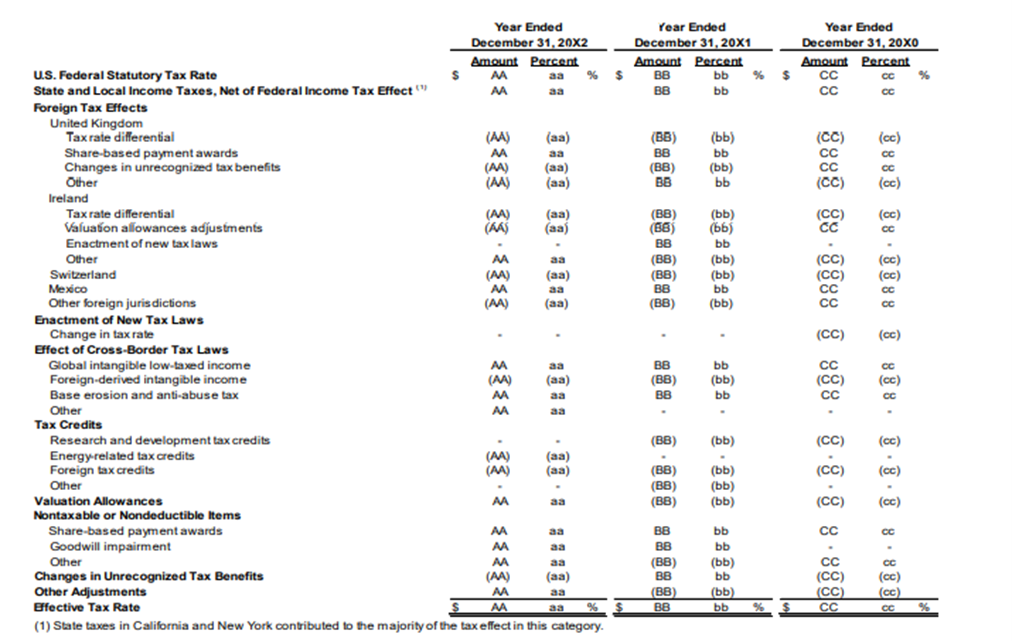

The ASU substantially expands out public company rate reconciliation reporting. Under the proposed update, public business entities will be required to disclose the following categories, within a tabular format, using both percentages and reporting currency amounts within their effective tax rate disclosure:

Furthermore, any reconciling items discussed below would be required to be separately broken out to the extent the impact is greater or equal to 5% of the amount computed by multiplying income (or loss) by the applicable statutory federal income tax rate. For entities parented in the U.S., this amount is effectively any item with an effect of 1.05% (21% US federal rate x 5%) or greater:

Finally, public business entities will be subject to certain qualitative disclosures in addition to the quantitative disclosures noted above. These include:

The proposed ASU provided the following public entity sample disclosures as an illustrative guide:

Private entities

Private entities are subject to less onerous reporting. The entities are only required to include qualitative disclosures in their financials statements that describe the items noted above but are exempt from the requirement of providing the quantitative disclosures.

Private entity disclosure example:

The difference between Entity W’s effective tax rate and its statutory tax rate is primarily attributed to tax credits, state taxes, and foreign taxes. More specifically, the foreign tax effects of Entity W’s operations in Ireland had a decreasing effect on its effective tax rate, while the foreign tax effects of Entity W’s operations in France had an increasing effect on its effective tax rate. Entity W received federal research and development tax credits, which decreased its effective tax rate, while state taxes in California increased its effective tax rate.

A&M Insight: While the amount of time to prepare disclosures under the proposed ASU may take more time in the past, Companies ought to have this level of detail readily available. Preparers of tax provisions should ensure that they are able to gather this information and start determining ways to appropriately disaggregate this within their existing provision models.

Under the existing codification, companies are required to disclose a single line item on their statement of cash flows enumerating the amount of cash paid for income taxes in a given reporting period. The proposed ASU provides for more granularity. Companies will be required to disaggregate cash paid (net of refunds received) for federal, state, and foreign taxes on both an annual and interim basis. Within the disaggregated line items, further disaggregation will be required to be made based on individual jurisdiction if the tax paid is 5% or more of the total balance of each category. The FASB’s proposed ASU subjects both public and private business entities to this change.

A&M Insight: Similar to the changes to the ETR, we expect Companies should generally have this level of detail available within their existing income tax provision schedules. Companies should ensure that they can readily produce this information to produce timely tax disclosures.

The proposed ASU incorporates items that have previously received public comment as part of its effort to improve disclosures surrounding income taxes:

A&M Insight: These changes largely align the ASC 740 codification with existing SEC regulations. As such, we do not anticipate that these changes would result in additional work for tax departments. Further, the elimination of certain unrecognized tax benefits disclosures we view as positive as there was diversity in practice of reporting and the requirement generally would not provide meaningful information to the financial statement readers.

In order to maintain comparability, the FASB has proposed that this ASU will be adopted on a retrospective basis. Therefore, companies will need to modify their comparative period disclosures to adjust for these changes in the period of adoption.

In contrast to prior simplification initiatives, the proposed changes to tax disclosures would require increased overall reporting efforts on behalf of companies and their advisors. Companies should assess their reporting processes to ensure that they are proper systems in place to gather this information in preparation of the final ASU upon adoption.

FASB encourages stakeholders to provide comments on the proposed ASU by May 30, 2023.

Please contact our experts if you have any questions on how these disclosure changes might impact your financial reporting process.