Publish Date

Mar 09, 2021

Special Tax Alert

On Saturday, the Senate passed H.R. 1319, the American Rescue Plan Act of 2021 (“Rescue Plan”), with a few notable amendments to the version passed by the House of Representatives. Due to those amendments, the legislation now returns to the House for another vote before heading to the President’s desk to be signed into law. Because the Senate’s amendments appear to have been negotiated in advance by the two chambers and the White House, the amended Rescue Plan is expected to clear the House without any issues and to be signed into law by the Democrats’ self-imposed deadline of March 14, in order to prevent a lapse of unemployment benefits.

This alert highlights some of the key tax law provisions included in the version of the Rescue Plan passed by the Senate, including the following:

Employment Tax Provisions

The Rescue Plan would modify some of the employment tax provisions created by the Families First Coronavirus Response Act (“FFCRA”) and the CARES Act, which were subsequently extended or enhanced by the Consolidated Appropriations Act, 2021 (“CAA”). The Rescue Plan, as amended by the Senate, would also exempt certain unemployment benefits from taxation.

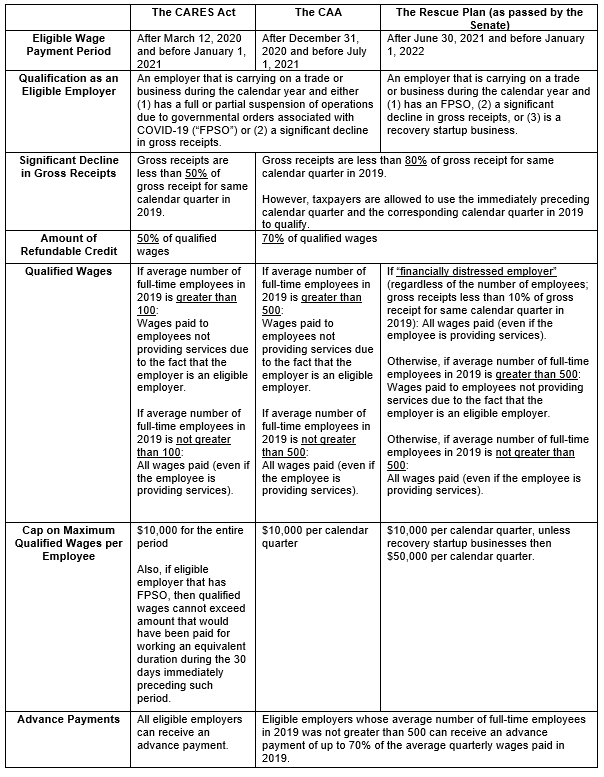

Employee Retention Credit

The employee retention credit (“ERC”) is a refundable credit equal to a percentage of the qualified wages paid by an eligible employer. The ERC was created by the CARES Act and later expanded by the CAA. The Rescue Plan would extend the ERC by two calendar quarters, making it applicable to qualified wages paid from July 1, 2021 through December 31, 2021. It would also expand the universe of employers eligible to receive the credit to include so-called “recovery startup businesses.” Recovery startup businesses are new businesses that began operations after February 15, 2020, have average annual gross receipts of $1 million or less during the three-taxable-year measurement period, and would not otherwise qualify as an eligible employer (as discussed below). The following table highlights the rules governing the ERC under the two laws and the Senate’s version of the Rescue Plan:

In addition, the Rescue Plan would make the ERC refundable against the employer share of Hospital Insurance tax (“Medicare tax”), instead of against the employer share of the Social Security tax, after June 30, 2021. This change would ensure that the maximum ERC is no longer reduced by certain other credits, including those allowed for qualified veteran employment and for qualified small business research expenditures. However, under the Rescue Plan, the definition of qualified wages does not include certain wages that are taken into account in determining certain credits, including the research credit under section 41 and the work opportunity credit under section 51.

A&M Insight: Fortunately, the CAA retroactively allowed employers to qualify for both the ERC and forgivable Paycheck Protection Program loans (although the loans cannot be used to pay qualified wages for which the ERC is being claimed). However, as highlighted above, the computation and benefits afforded by the ERC vary based on the period the wages are paid and the size of the employer. The ERC continues to pose quantitative and qualitative complexities that employers will need to overcome to ensure that they are properly calculating their ERC. A&M would be happy to discuss your particular situation and help address your questions.

Paid Sick and Family Leave and Associated Credits

As discussed previously, under the FFCRA employers with fewer than 500 employees were required to provide expanded Family and Medical Leave Act (FMLA) paid leave and paid sick leave related to COVID-19 through December 31, 2020. The FFCRA provided payroll tax credits to employers to partially cover expenses associated with such leave.

Under the CAA, employers are allowed to continue to provide FFCRA paid leave on a voluntary basis through March 31, 2021, and if they do, they will continue to receive the associated FFCRA payroll tax credits. The Rescue Plan would extend the now-voluntary FFCRA paid leave (and resulting payroll tax credits) through September 30, 2021.

In addition to extending the FFCRA paid leave and payroll tax credits, the Rescue Plan would make a number of other noteworthy changes, including:

These changes would generally become effective for FFCRA wages paid after March 31, 2021. However, for self-employed individuals, the changes would be effective as of January 1, 2021.

A&M Insight: Although the Rescue Plan does not reinstate the employer mandate to provide FFCRA paid leave, that issue has not been foreclosed. The Biden Administration has shown interest in restoring the mandate (or, at least, a mandate), and there are a number of more comprehensive paid leave proposals, such as the FAMILY Act (S. 248), which may receive consideration later this year.

Unemployment Compensation

Under the Rescue Plan, up to $10,200 in unemployment compensation would be exempt from taxation for individuals with adjusted gross income (AGI) of $150,000 or less. This special rule would be applicable for taxable years beginning in 2020 only.

Business Tax Provisions

While the Rescue Plan achieves its tax-and-spending outcomes primarily through deficit spending, it does include four revenue raisers that may have implications for many businesses.

Expansion of Deduction Limits for Highly Compensated Employees

Under section 162(m), as modified by the Tax Cuts and Jobs Act, publicly held corporations may not deduct wages or other compensation in excess of $1 million paid annually to the CEO, CFO, or the three highest-paid non-CEO or CFO employees. The Rescue Plan would expand this deduction limitation by five employees – to include the top eight highest-paid employees, plus the CEO and CFO. The change would take effect for taxable years beginning after December 31, 2026.

Repeal of Worldwide Interest Allocation

Under current law, 2021 is the year in which existing U.S. affiliated groups have to decide whether they want to switch from water’s-edge to worldwide allocation and apportionment of interest expense. The provision, which was enacted in 2004 originally to become effective for taxable years beginning after 2008, has been delayed numerous times. If the provision were to remain in force, those wishing to switch to worldwide allocation and apportionment under section 864(f) would be required to elect that treatment for their first taxable year beginning after December 31, 2020. While the election would be irrevocable without the Secretary’s consent, due to the lack of final regulations, many commentators had been hoping that preliminary guidance would be issued to give taxpayers a little more wiggle room in terms of timing. The Rescue Plan would repeal the availability of the election and maintain the status quo for allocation and apportionment of interest expense.

A&M Insight: Repeal of worldwide interest allocation may increase taxes on worldwide affiliated groups that are relatively highly leveraged outside the United States. However, considering that section 864(f) was added to the Code in 2004, its effective date was deferred several times, and the section saw the intervening enactment of the TCJA, it is unclear how many taxpayers had been planning to take advantage of the election. That said, some commentators were surprised that the relief package would repeal the election permanently, rather than delay its effective date once more. However, the proposed repeal of the election did not face much opposition from lawmakers during either House or Senate consideration, and as one of Democrats’ few revenue raisers in the relief bill, delay or repeal of the section 864(f) election always seemed likely once it was proposed.

Reduced Reporting Thresholds for 1099-K Income

The Relief Plan will increase compliance costs by lowering the threshold to trigger the requirement of a third-party settlement organization to report to its network participants on a Form 1099-K. Third-party settlement organizations include gig economy companies, such as Uber and Lyft, as well as online payment processors, such as PayPal.

Specifically, the proposal would reduce the threshold from more than $20,000 in aggregate payments and at least 200 transactions to more than $600 in payments, regardless of the number of transactions. The modified reporting threshold would be effective for calendar years beginning after December 31, 2021.

A&M Insight: The volume of payments being handled by third-party settlement organizations has increased dramatically over the past decade with the proliferation of gig work and other independent work arrangements. Perhaps owing to the increase in these work arrangements, recent TIGTA reports have highlighted the pervasive underreporting of 1099-K income and other related taxpayer compliance issues. Policymakers are well aware of the rampant noncompliance the current reporting thresholds enable, and bipartisan support exists for lowering the 1099-K reporting threshold. The only difference between the parties is that Republicans have generally called for pairing worker classification safe harbors with any changes to the information reporting requirements.

Excess Business Loss Limitation Extended Through 2026

Under the TCJA, non-corporate taxpayers may not use trade-or-business losses to offset more than $500,000 in nonbusiness income for taxable years beginning after December 31, 2017 and before January 1, 2026. The CARES Act repealed this limitation for taxable years beginning before January 1, 2021, allowing pass-through entities and sole proprietorships to offset, and potentially carry back, their losses to the extent of any nonbusiness income in taxable years 2018, 2019, and 2020.

The Rescue Plan would extend the limitation by one year – through taxable years beginning before January 1, 2027 – while leaving untouched the relief provided by the CARES Act.

A&M Insight: The relaxed rules under the CARES Act governing excess business losses have been under attack by progressive lawmakers since day one. While the Rescue Plan extended the time period during which the use of business losses to offset nonbusiness income is limited, it is unlikely that this change will satisfy the lawmakers who have been calling for retroactive repeal of the CARES Act provisions for months. Therefore, additional modifications may be featured in future Democratic tax bills.

A Third Round of Stimulus Payments

The Rescue Plan would provide individual taxpayers an advance refundable income tax credit against their 2021 tax liability in the amount of $1,400 ($2,800 for joint returns), increased in either case by $1,400 for each dependent of the taxpayer.

The Senate’s version of the legislation adopts stricter income eligibility requirements (and correspondingly faster phaseouts) than those included in the House-passed bill or those imposed by the CAA. Specifically, the amount of the credit would be reduced (but not below zero) by 28% (i.e., by $28 for every $100) of the taxpayer’s AGI that exceeds:

For taxpayers with dependents, consistent with the previous rounds of direct payments, the thresholds are slightly higher.

A&M Insight: Moderate Senate Democrats, such as Sen. Joe Manchin, successfully lobbied for more targeted stimulus payments, which resulted in the Senate’s rejection of the House-passed Rescue Plan’s significantly higher phaseout thresholds. However, despite the Senate’s changes, this round of direct payments is still the most generous round of payments yet. For example, under the Rescue Plan, college-age and other adult dependents would be able to qualify for a stimulus payment.

Noticeably Absent Provisions

Some of the provisions missing from the Rescue Plan are just as interesting as the provisions included in it. The Rescue Plan would not repeal the CARES Act’s net operating loss provisions, nor would it repeal the TCJA’s $10,000 cap on state and local tax deductions. Although Senate Majority Leader Chuck Schumer has called for lifting the SALT cap, President Biden has remained quiet on the issue. However, Biden Administration officials, including Treasury Secretary Janet Yellen, have left the door open for future action.

A&M Insight: These proposals will likely be considered should Democrats pursue their own version of tax reform later this year. As discussed previously, Democrats may use reconciliation to pass not one, but two tax bills this year, which means a second partisan measure is all but guaranteed. A&M expects tax to continue to be a central component of many pieces of legislation and would be happy to discuss how the proposals described above as well as other tax law proposals currently under consideration may affect you.

A&M Tax Says

Much like The Offspring’s classic track “Come Out and Play,” congressional Democrats are hoping their historic economic stimulus package, the second largest in American history, will help the U.S. economy come out of the doldrums caused by the coronavirus pandemic and stay open for business once and for all. This alert highlights just a few of the items within the Rescue Plan. As mentioned above, the Rescue Plan is based largely on the House-passed version of the legislation, with a few notable modifications. The House expects to vote on and pass the Senate’s Rescue Plan as soon as today. Please contact your trusted A&M Tax adviser if you have any questions regarding the Rescue Plan, including how it applies to your particular situation. Because much of the relief proposed in the Rescue Plan is limited in duration, the time to act is now.