Publish Date

Mar 04, 2025

A&M Tax Advisor Weekly

IRC Section 162(m) limits publicly held corporations to deducting no more than $1 million in compensation per taxable year for certain covered employees. Originally, Section 162(m) applied to the CEO, CFO and the top three highest-paid executives — generally the named executive officers. The 2017 Tax Cuts and Jobs Act (TCJA) amended Section 162(m) to include the concept of “once a covered employee, always a covered employee,” among other changes. Under this concept, once an employee is considered to be a covered employee for any taxable year after December 31, 2016, they will remain a covered employee, and their compensation will always be subject to the Section 162(m) deduction limitation. The 2021 American Rescue Plan Act (ARPA) further expanded the definition of covered employees to include the next five highest-compensated employees, effective for taxable years beginning after December 31, 2026.

The IRS recently released proposed regulations (REG-118988-22) [1] which provide further guidance on ARPA’s expanded definition of covered employees. The proposed regulations outline the methodology which would be used to identify the expanded group of covered employees. Additionally, the proposed regulations address the identification of covered employees at affiliated groups. A&M understands that many taxpayers may have questions about the interplay between the legacy Section 162(m) rules and the newly proposed regulations. Accordingly, this article summarizes the new regulations and provides a practical approach for managing the multiple categories of covered employees.

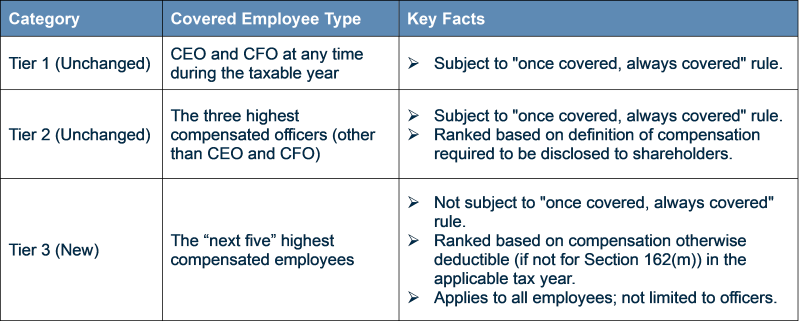

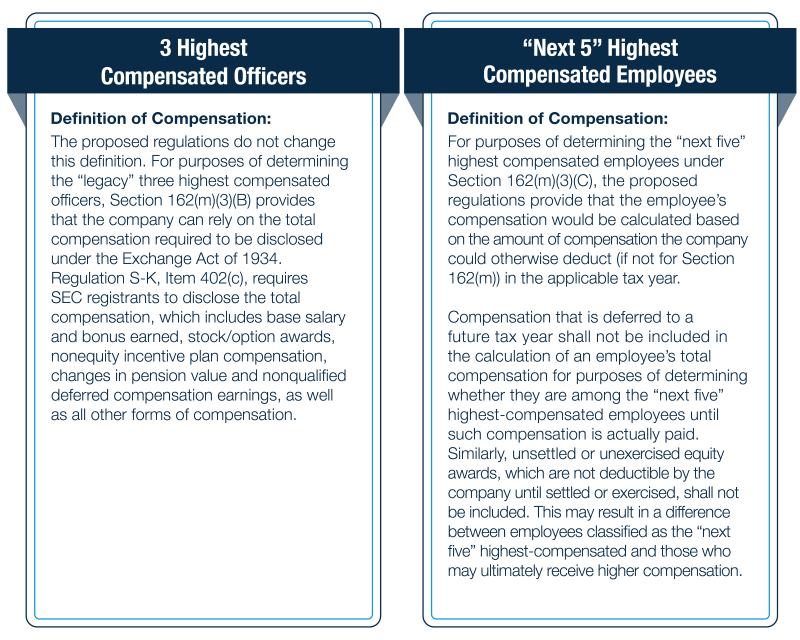

In tax years beginning after December 31, 2026, the definition of covered employees under Section 162(m) will expand. In addition to the CEO, CFO and the three highest-compensated officers, the “next five” highest-paid employees will also be considered covered employees. The rules for determining the CEO, CFO and the three highest-compensated officers remain unchanged (ranked based on the definition of compensation required to be disclosed to shareholders — practically, a “summary compensation table” definition). The “next five” highest-compensated employees will be subject to slightly different rules, including an annual review of their status (not subject to the “once covered, always covered” rule) and a different definition of compensation for purposes of ranking and identifying the “next five” employees. Accordingly, beginning in 2027, most publicly traded companies would have at least 10 covered employees under Section 162(m).

Covered employees can be categorized into three distinct tiers as summarized below:

Interplay Between “Legacy” Covered Employees and the “Next 5” Covered Employees

The proposed regulations define the “next five” covered employees as the five highest compensated employees for the taxable year other than the CEO, CFO or three highest compensated officers. Accordingly, the “next five” covered employees are determined independently from the CEO, CFO and three highest compensated officers. That is, there would be no overlap in these populations.

However, the proposed regulations do clarify that individuals already on the “once covered, always covered” list of covered employees (to the extent they are not currently the CEO, CFO or among the three highest paid officers) would be counted as one of the “next five” highest compensated employees based on their deductible compensation. Practically, this could shield employees from being pulled into the “next five” category.

The proposed regulations clarify that, for purposes of identifying the “next five” highest-compensated employees, the term “employee” is defined as it is in Section 3401(c), which includes both common law employees and corporate officers. This includes not only employees of the publicly held company but also employees of any member of the company’s “affiliated group.” Any employee who worked for the company during the applicable taxable year will be considered an “employee” for Section 162(m) purposes, even if they are no longer employed on the last day of the taxable year. For companies that use a professional employer organization or a similar entity to engage employees, the proposed regulations specify that employees providing services to the company will be treated as the company’s “employees” under Section 162(m). Under the proposed regulations, independent contractors appear exempt from Section 162(m); however, public companies should stay alert to potential IRS updates.

The proposed regulations expand the reach of the Section 162(m) rules pertaining to affiliated groups, as summarized below:

Comments on the proposed regulations are due by March 17, 2025.

The evolution of IRC Section 162(m) has expanded the scope of covered employees subject to the $1 million deduction limit. To ensure compliance and effective planning, A&M recommends that companies review and assess the impact of the proposed regulations before they take effect in the 2027 tax year. While this provides time for tax planning and adjustments to compensation structures, the impact on future compensation arrangements could be significant. Additionally, companies should consider the impact to deferred tax asset forecasts. As Section 162(m) continues to evolve, corporations must pay close attention to the key considerations and potential pitfalls mentioned above to maintain compliance with its rules.

If you have any questions, please do not hesitate to reach out to the Compensation and Benefits professionals at Alvarez & Marsal. We are uniquely qualified to help both corporations and individuals assess the reach and impact of Section 162(m). Our expertise gives us the ability to provide comprehensive guidance on how this regulation affects compensation strategies and reporting obligations.

[1] Federal Register, “Certain Employee Remuneration in Excess of $1,000,000 Under Internal Revenue Code Section 162(m),” Proposed Rule, January 16, 2025, https://www.federalregister.gov/documents/2025/01/16/2025-00728/certain-employee-remuneration-in-excess-of-1000000-under-internal-revenue-code-section-162m