Publish Date

Feb 06, 2025

India Tax Update

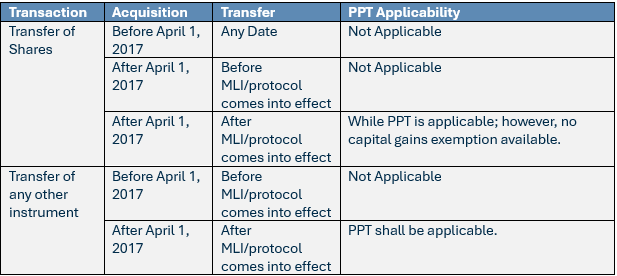

The Multilateral Convention to Implement Tax Treaty related provisions to prevent Base Erosion and Profit Shifting (MLI) entered into force for India on October 1, 2019. The MLI modifies India’s Double Taxation Avoidance Agreements (DTAAs). A key provision of the MLI is the Principal Purpose Test (PPT), which seeks to curb revenue leakage by preventing treaty abuse. The Principal Purpose Test enables denial of benefits under a DTAA where it is reasonably concluded that one of the principal purposes of an arrangement or transaction was to obtain a benefit, directly or indirectly, under a DTAA and that granting of the benefit is not in line with the object and purpose of the relevant provisions of the DTAA.

As per erstwhile DTAAs entered into with Mauritius, Singapore and Cyprus, capital gains tax arising on transfer of shares were taxable as per tax laws of such foreign jurisdictions. Amendment to the abovementioned treaties enabled India to tax capital gains arising on transfer of shares acquired after April 1, 2017 (source-based taxation). Accordingly, acquisitions prior to April 1, 2017, were grandfathered from capital gains tax in India.

While the Principal Purpose Test is included as an anti-abuse provision in India’s various DTAAs, either through the MLI or through bilateral processes, uncertainty remained on the applicability of PPT in case of grandfathered transactions.

The CBDT Circular No. 01/2025, issued on January 21, 2025,[1] intends to provide much-needed clarity on the scope and application of PPT including guidance on applicability of PPT in cases where grandfathering provisions are applicable under India’s treaties with Mauritius, Singapore and Cyprus.

Notes

a) Singapore: PPT for Singapore comes into effect from April 1, 2020. It is pertinent to note that the benefit of grandfathering is subject to satisfaction of limitation of benefit (LOB) clause and other specific tests under the India-Singapore DTAA.

b) Cyprus: PPT for Cyprus comes into effect from April 1, 2021. India-Cyprus DTAA does not have specific clause on LOB; accordingly, PPT shall be the only anti-abuse provision.

c) Mauritius: Although Mauritius has not ratified the tax treaty, the 2024 protocol proposing the addition of the PPT to the India-Mauritius DTAA created ambiguity regarding its prospective or retrospective application. This clarification confirms that PPT will not apply to grandfathered transactions. Additionally, the India-Mauritius DTAA does not include an LOB clause; accordingly PPT shall be the only anti-abuse provision.

The scope of GAAR is limited compared to PPT, applying only when (i) the main purpose is to gain a tax benefit, and (ii) it satisfies additional tests like arm’s length, commercial substance and bona fide purpose. Income tax rules exclude investments made before April 1, 2017, from GAAR. Consequently, transfer of shares acquired before this date are grandfathered under both PPT and GAAR.

CBDT clarifies that the application of PPT provision is expected to be a context-specific, fact-based exercise, to be carried out on a case-by-case basis, keeping in view the objective facts and findings.

Accordingly, the tax authorities cannot simply disregard the commercial rationale provided, and specific fact-based scrutiny ought to be carried out on a case-by-case basis before disallowing any benefit under the DTAAs.

The clarification is a significant relief for the investment and asset management community, which has been grappling with the uncertainty surrounding the interplay between the Principal Purpose Test and grandfathering provisions.

The clear demarcation of timelines alleviates ambiguity, affirming that the anti-abuse provisions of PPT shall be applicable only with prospective effect from the stipulated dates.

The clarity provided by the circular is a welcome respite for stakeholders, especially investors from Mauritius, Singapore and Cyprus, ensuring that grandfathered investments prior to the stipulated dates are not subjected to retrospective taxation. Accordingly, investors from Mauritius, Singapore and Cyprus selling shares of an Indian company that were acquired prior to April 1, 2017, continued to remain exempt in India under the grandfathering provisions.

While economic substance and commercial rationale remain critical for availing treaty benefits, the concern over retrospective application of PPT has been conclusively addressed. However, the applicability of the Principal Purpose Test to indirect transfers will require a detailed examination based on the interpretation of the relevant treaties.

[1] Government of India, Department of Revenue, “Circular No. 01/2025, Guidance for application of the Principal Purpose Test (PPT) under India’s Double Taxation Avoidance Agreements-rog.,” https://incometaxindia.gov.in/communications/circular/circular-1-2025.pdf