Publish Date

Apr 17, 2025

Asia Tax Update

On 28 March 2025, the State Taxation Administration (STA) of the People’s Republic of China (PRC) and the PRC Ministry of Finance (MoF) jointly published a prospect revision draft of the PRC Tax Collection and Administration Law (the Draft Revision), for the purpose of public consultation. The public consultation will run through 27 April 2025.[1]

As an important procedural law for adjusting the behaviour of tax collection, the Tax Collection and Administration Law is an essential legal framework for administering taxation in China. The current prevailing Tax Collection and Administration Law came into effect in 1993. It was then amended in 1995, comprehensively revised in 2001 and further amended through several articles in 2013 and 2015 in conjunction with the reform of the commercial system. The main topics covered by the PRC Tax Collection and Administration Law include taxpayer’s obligations, dispute resolutions, tax noncompliance liabilities, etc.

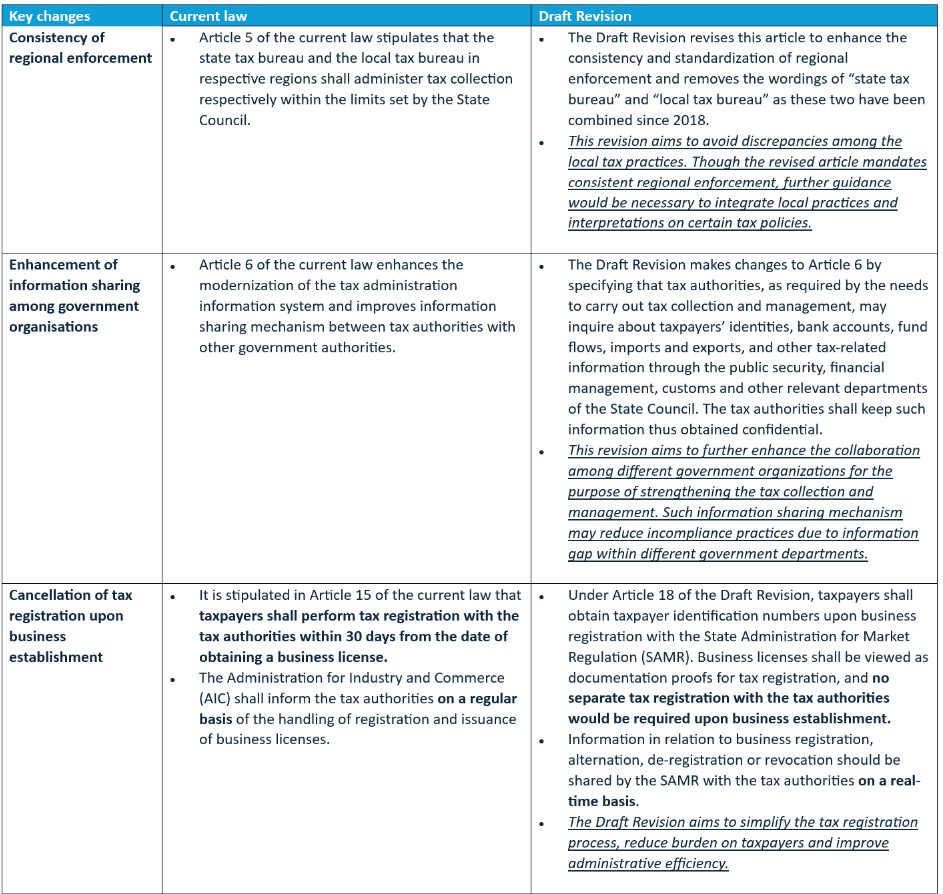

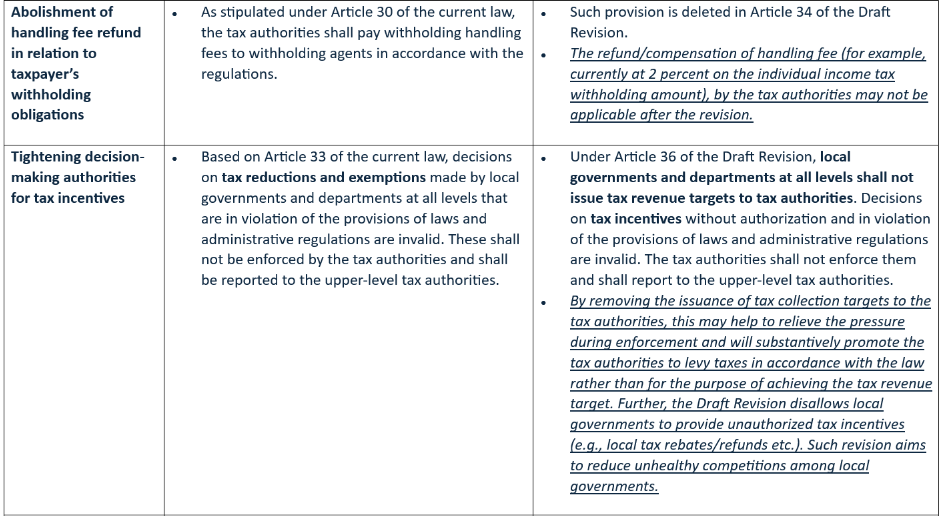

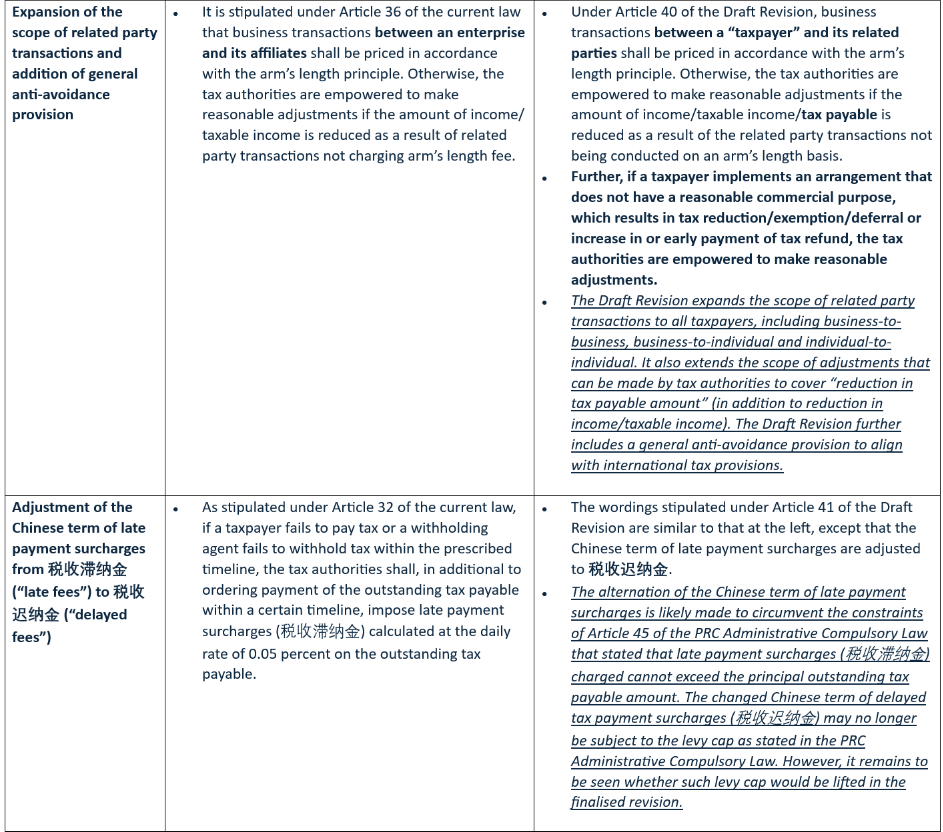

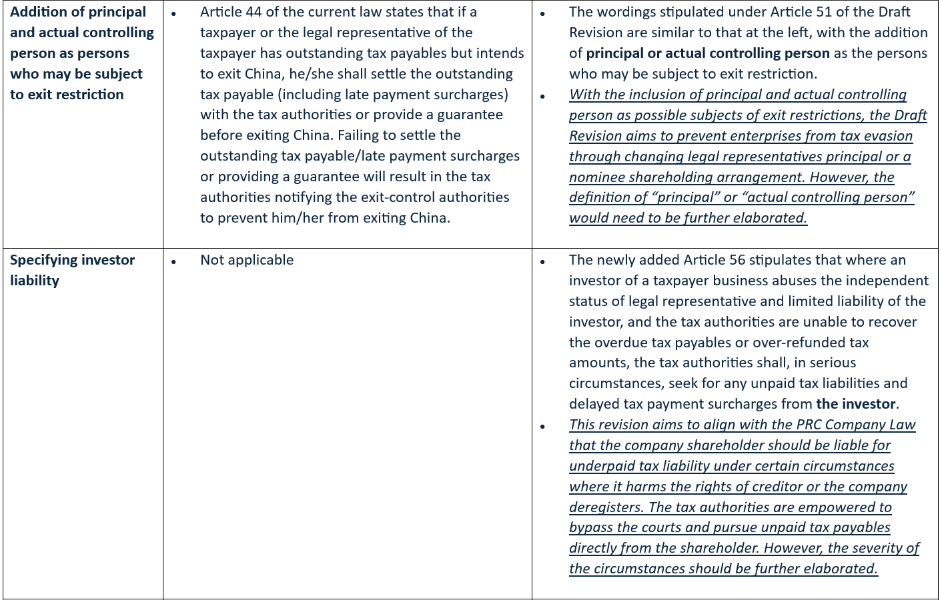

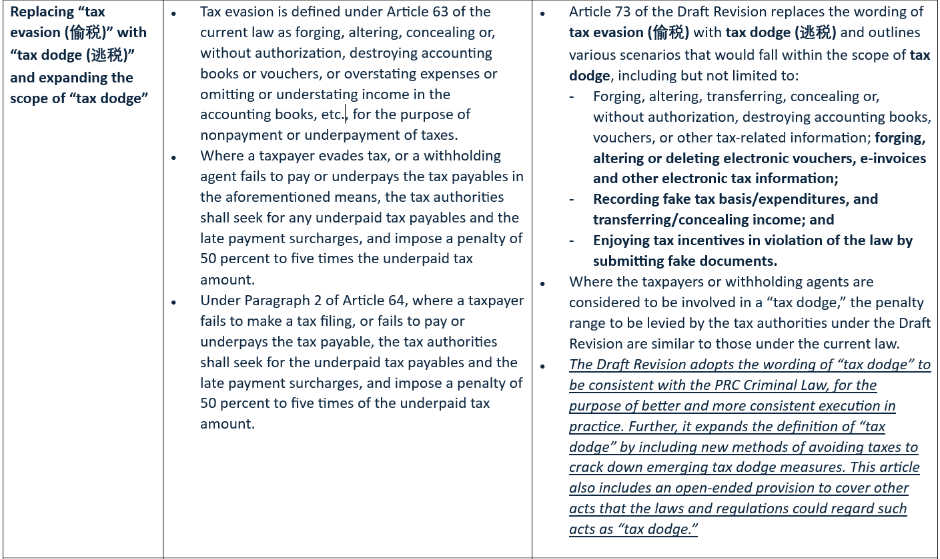

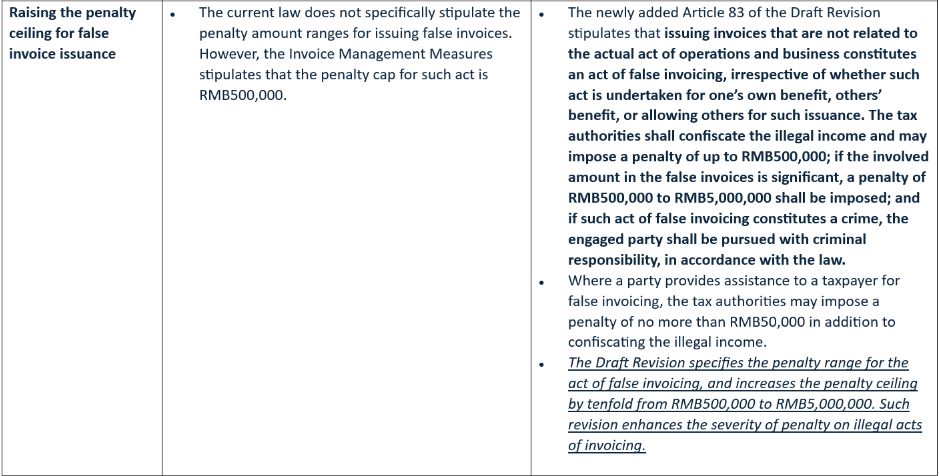

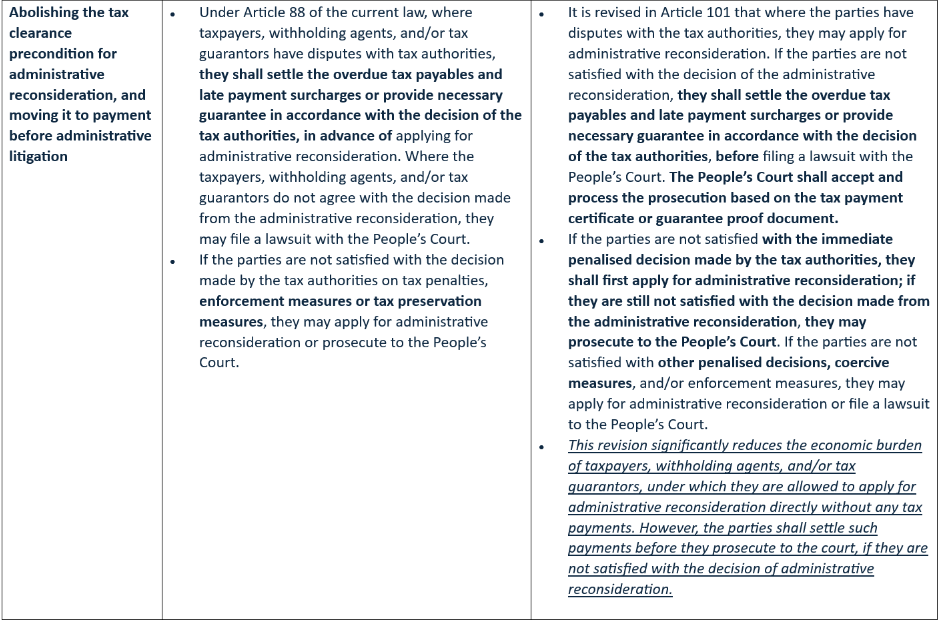

The current prevailing Tax Collection and Administration Law is organized across six chapters, comprising 94 articles. With the chapter setting structured as the current Tax Collection and Administration Law, the Draft Revision consists of 106 articles, with 16 new articles added, four deleted and 69 amended. Below is a summary of the key changes and their implications as outlined by the Draft Revision.

A comparison of the wordings of the key articles between the current law and the Draft Revision with our commentary is also set out in the table below.

Note: Please note that the above English version of the PRC Tax Collection and Administration Law and the Draft Revision is based on our translation, which is unofficial and for informational purposes only. It should not be used for any commercial activities by any other party.

In light of the key changes above, the Draft Revision aims to construct a more regulated and competitive taxation environment for businesses, by making efforts to improve the determination and confirmation of responsibility for illegal tax actions, providing more clarity on penalised measures, enforcing the protection of taxpayers’ rights, as well as accommodating the new trends of digital economy transition. However, certain highly demanded practical aspects, as aforementioned, are not included in the Draft Revision. Public comments are welcome, and more thoughtful amendments may need to be considered before the Draft Revision is finalised.

Alvarez & Marsal, a global professional services advisor, is committed to staying at the forefront of developments in tax legislation and sharing insights with businesses. With a team of experienced professionals, we assist businesses throughout every step of operation and transactions in identifying tax risks, negotiating with tax authorities, and improving compliance with the local tax practices in China and global market. If you have any opinion or feedback in respect of the proposed PRC Tax Collection and Administration Law, you may submit through the STA (https://www.chinatax.gov.cn) or MoF (http://fgk.mof.gov.cn) websites, or consult our team for assistance and coordination.

[1] “Law of the People’s Republic of China on the Administration of Tax Collection (Revised Draft for Comment) for Public Comment,” People’s Republic of China, 28 March 2025,

(《中华人民共和国税收征收管理法(修订征求意见稿)》公开征求意见),https://www.chinatax.gov.cn/chinatax/n810356/n810961/c5239263/content.html