Publish Date

Mar 20, 2024

Australia Bulletin

In this article, we provide an overview of the OECD Pillar 2 framework and the current status of the rules in Australia, and discuss some of the key implications and challenges for Australian taxpayers and tax practitioners.

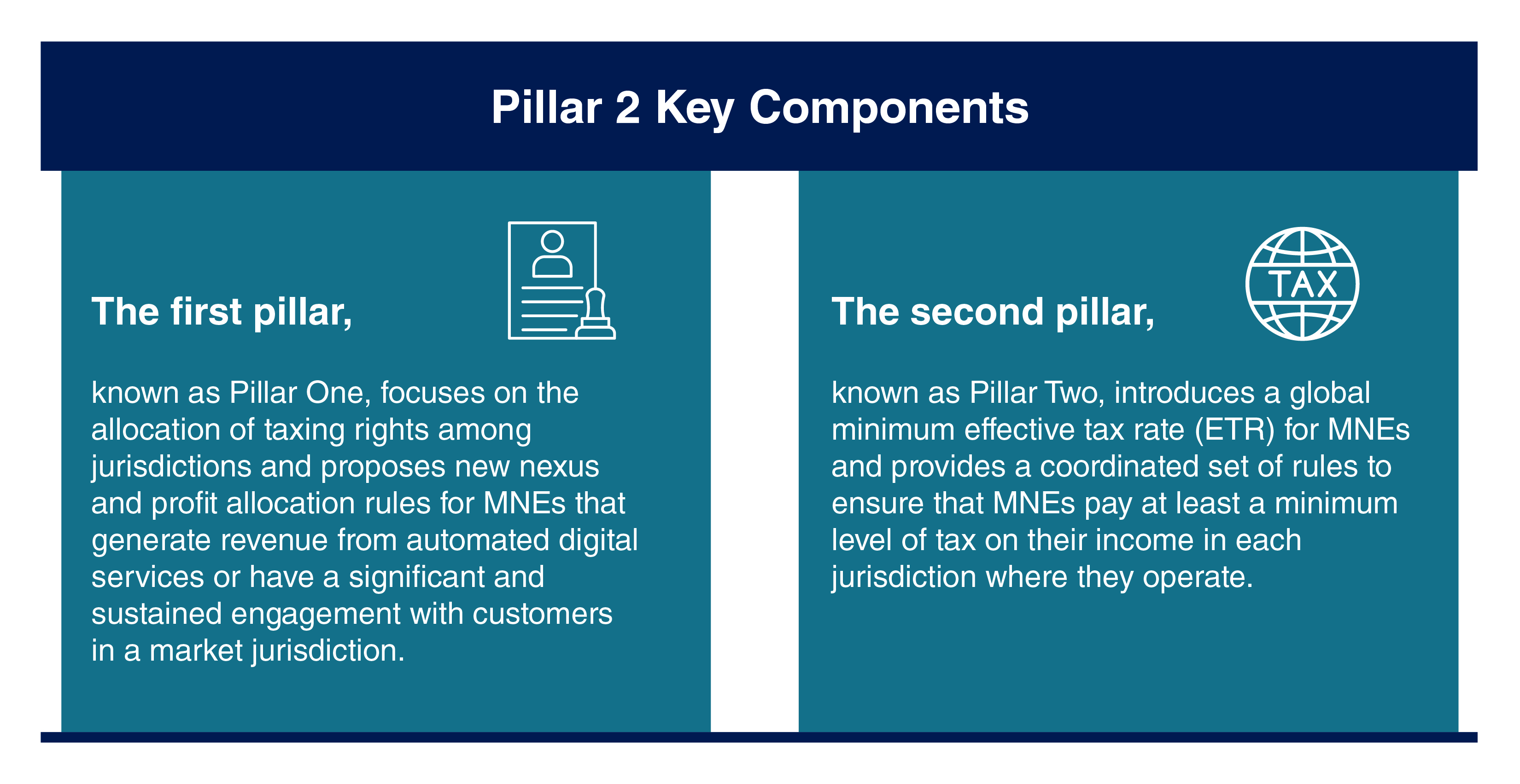

The Organisation for Economic Co-operation and Development (OECD) has developed a two-pillar solution to address the tax challenges arising from the digitalisation and globalisation of the economy. The two pillars aim to ensure that multinational enterprises (MNEs) pay a fair share of tax wherever they operate and create value, and to prevent the erosion of the tax base and the shifting of profits to low-tax jurisdictions.

The OECD has released a series of reports and guidance documents on the two-pillar solution, including the Model Rules on the Global Anti-Base Erosion (GloBE) Rules, which are the core component of Pillar Two. The GloBE Rules consist of four interlocking rules: the Income Inclusion Rule (IIR), the Undertaxed Payments Rule (UTPR), the Switch-over Rule (SOR), and the Subject to Tax Rule (STTR). The IIR and the UTPR are the primary rules that impose a top-up tax on the income of an MNE group that is taxed below the minimum rate in a jurisdiction, while the SOR and the STTR are secondary rules that limit the application of tax treaties and other tax benefits to low-taxed income.

The OECD has recommended that the two-pillar solution be implemented by more than 140 member jurisdictions of the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (BEPS) by 2023, with an effective date of 1 January 2024 for Pillar One and the IIR, and 1 January 2025 for the UTPR, the SOR and the STTR. The OECD has also suggested a minimum rate of 15 percent for Pillar Two, which was endorsed by the G20 Finance Ministers and Leaders in October 2021.

Australia is one of the jurisdictions that has committed to implementing the two-pillar solution in line with the OECD recommendations. In the 2023–24 federal budget, the Australian government announced that it will introduce legislation to implement the GloBE Rules and a Domestic Minimum Tax (DMT) of 15 percent, with effect from income years commencing on or after 1 January 2024. The DMT is a unilateral measure that will give Australia priority taxing rights over any low-taxed domestic income of an MNE group that is subject to the GloBE Rules.

The OECD Pillar 2 framework is designed to ensure that MNEs pay a minimum level of tax on their income in each jurisdiction where they operate, regardless of whether they have a physical presence or a taxable nexus there. The framework applies to MNE groups that have a consolidated accounting revenue of more than EUR 750 million (~AUD 1.2 billion) in the previous fiscal year, which is the same threshold as the Country-by-Country (CbC) reporting requirement under the BEPS Action 13. The framework does not apply to government entities, international organisations, nonprofit organisations, pension funds, investment funds or real estate funds, unless they control an MNE group that is otherwise in scope.

The framework consists of four interlocking rules that operate in a hierarchical manner: the IIR, the UTPR, the SOR and the STTR. The IIR and the UTPR are the primary rules that impose a top-up tax on the income of an MNE group that is taxed below the minimum rate in a jurisdiction, while the SOR and the STTR are secondary rules that limit the application of tax treaties and other tax benefits to low-taxed income. The following outlines the interaction of the four rules:

The IIR is the main rule that imposes a top-up tax on the income of an MNE group that is taxed below the minimum rate in a jurisdiction. The IIR applies to the parent entity of an MNE group, or any intermediate parent entity, on a top-down basis. The IIR requires the parent entity to include in its taxable income the proportionate share of the income of each entity in the MNE group that is subject to tax below the minimum rate in the jurisdiction where it is resident or where it carries on a permanent establishment (PE). The top-up tax is calculated by applying the difference between the minimum rate and the effective tax rate (ETR) of the entity to its income.

The ETR of an entity is determined by dividing the covered taxes paid or accrued by the entity by its income, as calculated under the GloBE Rules. The covered taxes include the corporate income taxes and similar taxes levied on the entity’s income by the jurisdiction where it is resident or where it has a PE, as well as any withholding taxes imposed on payments received by the entity. The income of an entity is calculated based on the financial accounting standards used by the parent entity for the preparation of the consolidated financial statements of the MNE group, with certain adjustments and exclusions. For example, the income of an entity excludes dividends and capital gains from the disposal of shares in entities that are part of the MNE group, as well as income that is subject to the STTR (discussed below).

The IIR applies on a jurisdictional basis, meaning that the ETR of an entity is calculated separately for each jurisdiction where it is resident or where it has a PE. The income and the covered taxes of an entity are allocated to the relevant jurisdiction based on the source and residence rules of that jurisdiction. The IIR also applies on a blended basis, meaning that the ETR of an entity is calculated by aggregating the income and the covered taxes of all the entities in the MNE group that are resident or have a PE in the same jurisdiction. This allows the MNE group to offset the income and the covered taxes of different entities within the same jurisdiction, and reduces the compliance burden and the volatility of the ETR calculation.

The IIR includes a de minimis exclusion that exempts an entity from the top-up tax if the total amount of income and covered taxes allocated to a jurisdiction is less than EUR 1 million (~AUD 1.6 million) or 2 percent of the MNE group’s total income, whichever is lower. The IIR also includes a substance-based carve-out that exempts an entity from the top-up tax if the entity’s income is derived from substantive economic activities in the jurisdiction where it is resident or where it has a PE. The substance-based carve-out applies if the entity’s payroll expenses and tangible assets in the jurisdiction exceed a certain percentage of its income in the jurisdiction, which is determined by applying a formula that takes into account the industry sector and the profitability of the entity.

The UTPR is a secondary rule that applies as a backstop to the IIR, in case the IIR does not fully capture the low-taxed income of an MNE group. The UTPR applies to any entity in an MNE group that makes a payment to a related entity that is subject to tax below the minimum rate in the jurisdiction where it is resident or where it has a PE. The UTPR requires the payer entity to either deny a deduction for the payment, or subject the payment to withholding tax, at a rate that is equal to the difference between the minimum rate and the ETR of the payee entity.

The UTPR applies to payments that are deductible for tax purposes in the jurisdiction of the payer entity, such as interest, royalties, service fees and rents. The UTPR does not apply to payments that are not deductible, such as dividends or payments that are subject to the STTR (discussed below). The UTPR also does not apply to payments that are made to an entity that is resident or has a PE in the same jurisdiction as the payer entity, or to payments that are made to an entity that is subject to the IIR in the jurisdiction of its parent entity or any intermediate parent entity.

The UTPR is subject to the same de minimis exclusion and criteria as the IIR.

The SOR is a secondary rule that applies as a backstop to the IIR and the UTPR, in case they do not fully capture the low-taxed income of an MNE group. The SOR applies to any entity in an MNE group that may be tax exempt in a jurisdiction where it has a PE. The SOR is aimed at scenarios where low-tax income arising in the PE jurisdiction may be blended with high tax income in the parent jurisdiction, thereby understating the amount of low-tax income in the PE jurisdiction and allowing the MNE to avoid a GloBE tax liability by sheltering low tax income with excess taxes paid in the parent jurisdiction.

According to the OECD, a parent entity that seeks to apply the income inclusion rule to the income of an exempt PE will, however, be prevented from doing so where the parent jurisdiction has entered into a bilateral tax treaty that obliges the parent jurisdiction to exempt the income. The aim of the switch-over rule would allow the state of the parent’s residence jurisdiction to apply an income inclusion rule to tax the income of the PE in those cases where the income inclusion rule would apply as a matter of domestic law.

The STTR is a treaty-based rule and a secondary rule that applies as a backstop to the other rules, in case they do not fully capture the low-taxed income of an MNE group. The STTR is a model treaty provision that allows jurisdictions to impose limited additional taxation on certain cross-border payments between connected companies where the recipient is subject to a nominal corporate income tax rate below 9 percent. The STTR applies to interest, royalties and a specified list of other payments (Covered Income), including all intra-group service payments.

The STTR applies to any entity in an MNE group that makes a payment to a related entity that is subject to tax below a certain threshold in the jurisdiction where it is resident or where it has a PE. The STTR requires the payer entity to subject the payment to withholding tax (i.e., tax on gross income) up to 9 percent but may be reduced to the difference between the threshold and the nominal tax rate of the payee entity.

The STTR applies only if the aggregate sum of Covered Income paid in a fiscal year exceeds EUR 1 million (or EUR 250 000 for jurisdictions with GDP below EUR 40 billion).

Australia is one of the jurisdictions that has committed to implementing the OECD Pillar 2 framework in line with the OECD recommendations. In the 2023–24 federal budget, the Australian government announced that it will introduce legislation to implement the GloBE Rules including :

The Australian government has stated that it will consult with stakeholders on the design and implementation of the GloBE Rules and the DMT, and that it will release an exposure draft of the legislation. However, as of the date of this article the draft legislation has not been released. The Australian government has also indicated that it will align the GloBE Rules and the DMT with the existing Australian tax rules and frameworks, such as the thin capitalisation rules, the controlled foreign company (CFC) rules, the hybrid mismatch rules and the diverted profits tax (DPT).

The Australian government has not yet announced its position on the SOR and the STTR, which are optional for jurisdictions to adopt. However, the Australian government has expressed its support for the multilateral instrument (MLI) that will be developed by the OECD to implement the STTR in the existing tax treaties. The Australian government has also stated that it will review its tax treaty network and consider renegotiating any tax treaties that do not reflect the OECD Pillar 2 framework.

The OECD Pillar 2 framework and the current status of the rules in Australia have significant implications for Australian companies, especially for those that are involved in cross-border transactions and operations with MNE groups. Some of the key implications and challenges are:

Controversy may also arise from consistency in the definition and measurement of the payments and the nominal tax rate of each entity in an MNE group, as well as the application and coordination of the MLI and the tax treaty negotiations.

This article has provided an overview of the OECD Pillar 2 framework and the current status of the rules in Australia, and discussed some of the key implications and challenges for Australian taxpayers and tax practitioners. The article is based on the information and guidance available as of February 2024, and may be subject to change as the rules are finalised and implemented. The article is not intended to provide legal, tax, or accounting advice, and readers can consult A&M further before taking any action based on the article. The article is also not intended to express any opinion or endorsement of the OECD Pillar 2 framework or the current status of the rules in Australia, and readers should form their own views and judgments on the rules. The article is solely for informational and educational purposes.

https://www.alvarezandmarsal.com/insights/oecd-pillar-2-framework-and-current-status-rules-australia