Publish Date

Feb 14, 2023

Human Capital Today

The Securities Exchange Commission (“SEC”) recently issued long-awaited final rules on Pay versus Performance (“PvP”) disclosure and clawbacks. These were mandated by the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”) that was passed in 2010 in response to the financial crisis. The SEC originally proposed the rules in 2015 and re-opened the comment period most recently in early 2022. The final rules add significant complexity to existing executive compensation proxy statement disclosure requirements and may pose a substantial administrative burden on companies.

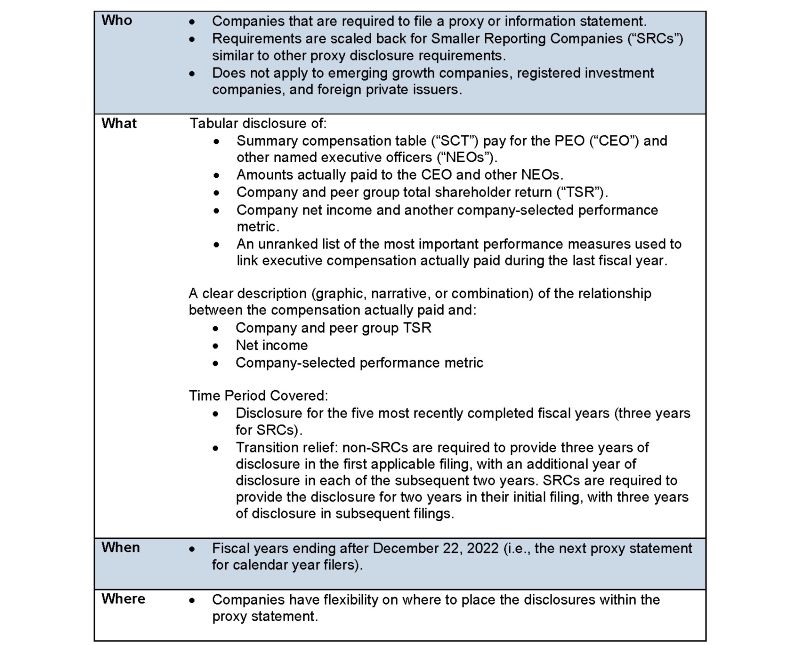

Below is a high-level snapshot of the disclosure-related effects:

The SEC prescribed the tabular format below:

While the tabular format will provide consistency and appears relatively straightforward, as they say, the devil is in the details.

To determine the amount of compensation “actually paid,” companies will start with the total compensation reported in the SCT, then make significant required adjustments, in particular for equity awards. For some companies, this may be the most challenging aspect of the PvP disclosure and will require a fair value determination of the equity awards at the end of each year. Companies will deduct the equity award amounts from the SCT total compensation, and add back the following:

Companies generally strive to have their long-term incentive awards be “equity-classified” for Generally Accepted Accounting Principles (“GAAP”) purposes, when possible, with a primary benefit being that the company determines the fair value of the award at the grant date and is generally not required to subsequently re-value the award. This treatment allows for a fixed compensation charge and less administrative burden. However, companies will now need to re-value their outstanding equity awards each year for the PvP disclosure and track accrued dividends if not accounted for in the fair value.

The determination of fair value as of the end of the year for time-vesting restricted stock or restricted stock units is generally straightforward. However, a fair value determination for performance-vesting awards and stock options is more time intensive and costly for companies. Companies that utilize a third-party valuation firm to value awards with performance measures such as relative TSR may now need to have the awards valued each year, rather than just at the grant date. In particular, the first year of disclosure will be extraordinarily burdensome on companies due to the number of calculations that will need to be performed in order to comply.

Another one of the more potentially burdensome requirements will be the disclosure of both the company and peer group TSR. While many companies already disclose TSR for themselves and their peer group in the Compensation Discussion & Analysis (“CD&A”) narrative, the PvP disclosure requirements attempt to standardize the methodology by requiring companies to calculate TSR based on a fixed initial $100 investment. Companies will then have to disclose the relationship between the company’s TSR and that of the peer group.

Once again, the devil is also buried in the details of this requirement. When compiling the peer group TSR, which is required to be disclosed as an average in the PvP table, companies are required to weight the peer group average based on the market capitalization of the companies, a significant complexity that many, if not all, companies are not currently undertaking in their disclosures.

And while the peer group will generally be the same as that disclosed in the CD&A as part of the description of the company’s benchmarking practices, if the peer group for PvP purposes differs, or if the peer group is not a published industry or line-of-business index, the company must identify the list of companies comprising the peer group in a footnote to the PvP table. Further, if a company changes the peer group used in the PvP disclosure from that used in a prior year, while it is only required to include the peer group TSR of the new peer group in the tabular disclosure, it is required to include a footnote explaining the reason for the change in the peer group as well as compare the company’s TSR to both the old and new peer group. In such instances, a company must not only track and calculate the TSR of the current peer group, but any prior peer groups utilized in previous PvP disclosures of the prior five reporting year periods, a potentially significant burden for many companies that could influence decisions of whether or not to adjust their compensation peer group.

For non-SRCs, this also requires additional disclosure of a “company-selected measure” (“CSM”) which, along with being another helpful acronym for compensation professionals, is the “most important financial performance measure” used to link compensation actually paid to the NEOs for the most recently completed fiscal year. The performance under this metric must be shown for each covered fiscal year, and the company must provide a clear description (graphic, narrative or both) of the relationship between the executive compensation actually paid and this CSM. Because most companies utilize a variety of metrics to determine executive compensation, companies can provide supplemental disclosure of additional metrics and/or cross-reference to other areas of the proxy statement that disclose the process and calculations that go into determining NEO compensation.

But wait, there’s more. Non-SRC companies must include another tabular disclosure that provides an unranked list of three to seven financial performance measures that represent the most important financial performance measures used by the company to link compensation actually paid to the NEOs for the most recently completed fiscal year. In some instances, non-financial measures can be included as well.

This will certainly be an area of the PvP disclosure that requires coordination between company management and the compensation committee.

The SEC also adopted final rules that direct national securities exchanges to adopt listing standards requiring listed issuers to develop and implement a clawback policy. The required clawback policy must provide for recovery, in the event of an accounting restatement, of incentive-based compensation received by current or former executive officers. Companies must also file the clawback policy as an exhibit to their annual report and include additional disclosures in the event a clawback is triggered under the policy.

To comply with the rules, the clawback policy must be triggered in the event an issuer is required to prepare an accounting restatement—including to correct an error that would result in a material misstatement if the error were corrected in the current period or left uncorrected in the current period. If the policy is triggered, the company will have to recover any incentive-based compensation that was erroneously awarded during the three years preceding the date the restatement was required to any current or former executive officer.

The SEC’s rule provides that the listing exchange require adoption of a compliant clawback policy or face delisting from the exchange. However, unlike the PvP rules, companies have a longer runway to achieve compliance. Exchanges must propose the listing standard policy no later than 90 days following the rule’s publication in the Federal Register, listing standard policy must be effective no later than one year following the publication date, and each issuer will be required to adopt a compliant clawback policy no later than 60 days after the effective date.

While the intent of the PvP disclosures is to provide investors with transparent, comparable and understandable disclosure of a company’s executive compensation, the reality for companies will be added complexity, cost and administrative burden. Further, these additional SEC disclosure requirements will add to the ever-growing length of the proxy CD&A, potentially crowding out key narratives and discussions in favor of the required disclosure tables. Lastly, final rules related to clawback policies also may require additional action by companies and their boards. As such, publicly-traded companies should begin gathering the information required for the PvP disclosure and start the related conversations with their compensation committees soon in order to be ready for the upcoming disclosures.