Publish Date

Mar 05, 2024

Expertise

While there is considerable buzz these days surrounding the Federal Section 48 Investment Tax Credit (ITC), it is worth noting that many states have their own versions. These tax credits are usually simpler to claim, and, in most cases, regular capital spend will qualify. Taking advantage of these programs can help accelerate growth and position a company for long-term success. Here is a breakdown of how these programs can benefit companies along with three state-specific examples.

Investment tax credits can play a pivotal role in fueling business expansion and attracting investment. These credits provide businesses with financial incentives to invest in designated regions or industries, thereby stimulating economic growth. By capturing these credits, companies can allocate capital towards expansion projects, such as facility upgrades, equipment purchases, research and development (R&D) initiatives or workforce training programs. The availability of investment tax credits reduces the upfront costs associated with these investments, making them more feasible and attractive to businesses.

In many instances, these types of tax credits come with enhancements that allow companies to take a larger credit if they create new jobs or hit certain investment targets. By incentivizing companies to engage in capital spending, states hope to create increased employment opportunities and workforce growth. Businesses taking advantage of these credits not only benefit from cost savings but also contribute to job creation and local economic stability.

Many states offer investment tax credits that target specific industries or sectors they wish to promote. By focusing on these industries, states can encourage technological advancements, innovation and competitiveness. We have seen this most recently in the semi-conductor and automotive (EV) sectors. Businesses that operate within identified sectors can leverage investment tax credits to fund research and development projects, improve production capabilities, drive innovation or invest in additional training for its workforce. By focusing growth on strategic industries, states can enhance their overall economic landscape and position themselves as attractive locations for companies looking to expand, relocate or build greenfield facilities.

Illinois is a perfect example of a statutory, zone-based ITC. For companies located within an Illinois Enterprise Zone (EZ), a five percent credit against state income tax is allowed for investments in qualified property. Qualified property is tangible property, including buildings and structural components, that is depreciable, and has a useful life of four or more years. In this scenario, a company will receive a tax credit for regular, yearly capital spend so long as the location is within an EZ. There are over 90 Illinois Enterprise Zones.

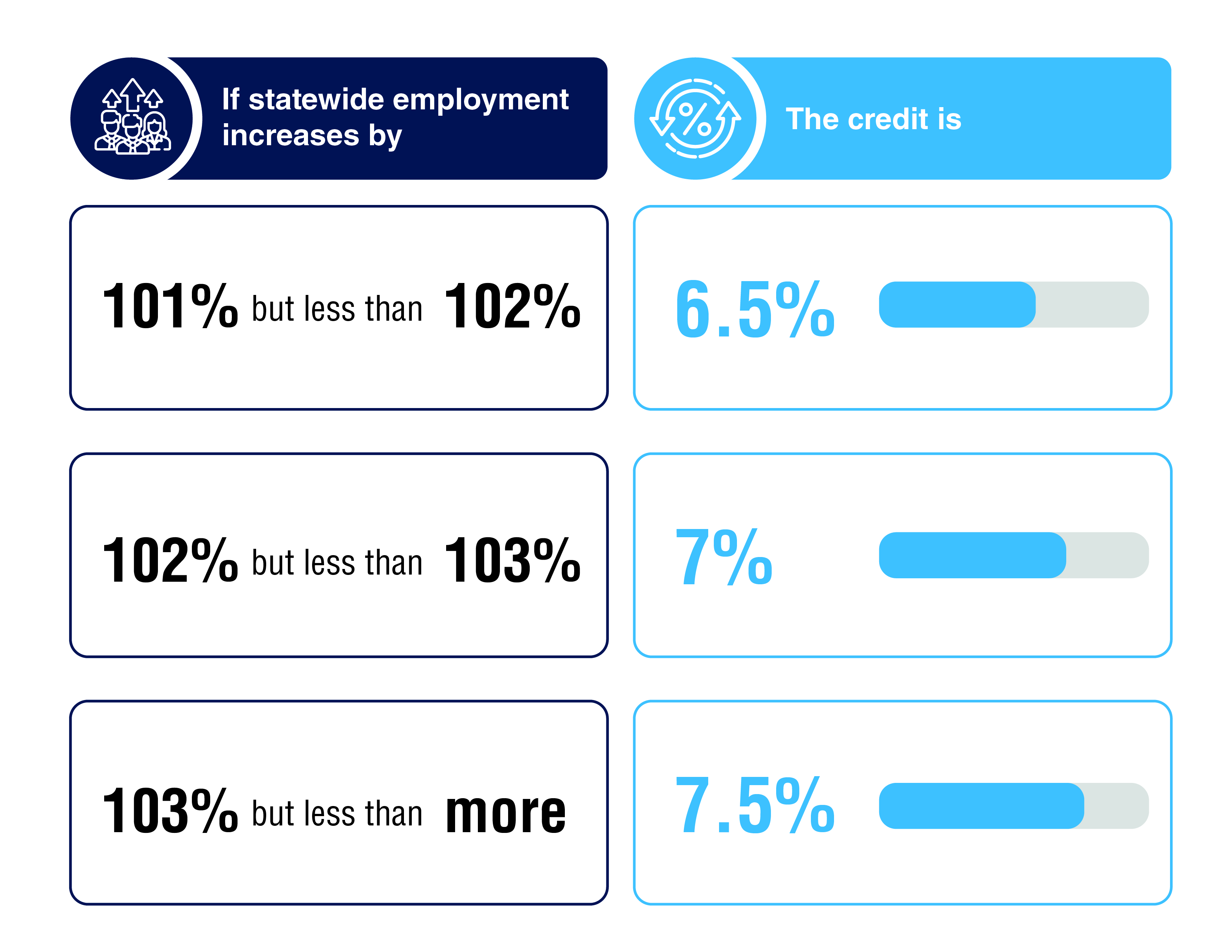

New York has an ITC like Illinois but with two important distinctions. First, it is not zone based so companies who are investing in facilities in New York will qualify for the credit automatically. Second, there are enhancements available to companies that also increase their statewide headcount. The credit is five percent on the first $350,000,000 in investment and four percent for any amount more than $350,000,000. For companies that increase their statewide employment the credit can be enhanced as follows:

|

|

There is also an optional R&D ITC that allows companies to take a nine percent tax credit on R&D related property.

The South Carolina ITC is an example of an industry-specific program. Credit is allowed for manufacturers who are locating or expanding in the state. It is a one-time credit against a company’s corporate income tax rate of up to 2.5 percent of a company’s investment in new production equipment. The value of the credit is dependent on the recovery period for the property placed in service and is as follows:

In conclusion, utilizing ITCs can have a significant impact on a company’s bottom line, fund additional expansions and increase production capabilities. Many of these programs incentivize annual capital spend. Identifying the most suitable programs for your company and industry presents a complex challenge in unlocking valuable credits. A&M offers expertise to not only assist you in qualifying for and optimizing these benefits but also manages the intricate administrative tasks associated with the programs to safeguard against missing out on potential advantages. To delve deeper into how we can support you, we invite you to contact one of our RCIS professionals for a consultation.